This analysis is for informational and educational purposes only and is not intended to be read as investment advice. Click here to read the full disclaimer.

BHP's $40 billion takeover offer for Anglo American is primarily about copper. But a successful deal would make BHP an even bigger metallurgical coal miner as the long-term outlook for steel products worsens and investor pressure on Scope 3 emissions increases.

In a statement to the ASX, BHP said: “The combined entity will be a large-scale, low-cost, long-lived company focused on future-proof commodities such as iron ore, metallurgical coal, potash and copper. “We will have a major portfolio of Tier 1 assets.”

If the bid is successful, Australia's second largest exporter of metallurgical coal will become the largest producer. BHP has been highly critical of the renewal of Queensland's coal fees, but now appears to be in favor of adding Anglo coal mines in the state.

It is possible that BHP may seek to spin off its expanded coal business at some point in the future. Nevertheless, as it stands, the takeover proposal includes the separation of Anglo's South African Iron Ore (Kumba Iron Ore Ltd) and Platinum Group Metals (Amplats) businesses. Other Anglo businesses, including De Beers, will be subject to a strategic review upon completion.

BHP has recently been transferring its low-grade metallurgical coal mines to the likes of Whitehaven Coal, believing that steelmakers will gravitate towards higher quality as they seek to reduce emissions from blast furnaces. Anglo's Queensland mines produce strong coking coal, which BHP is keen to produce.

BHP's hopes that demand for hard coking coal will continue for decades to come, at least in part, because carbon capture, utilization and storage (CCUS) is key to decarbonizing blast furnace-based steelmaking and sustaining demand for metallurgical coal. It is based on the company's continued belief in playing a vital role. . This is despite a wealth of evidence to the contrary.

IEEFA's new report on CCUS for the steel industry finds that steel manufacturers are increasingly turning to better alternative technologies such as direct reduced iron (DRI), and the poor performance of carbon capture technologies has led to major emissions reductions. It turns out that the role of reduction is becoming increasingly unlikely.

There are no commercial-scale CCUS plants for coal-based steel manufacturing anywhere in the world, and there are almost none in the pipeline.

German think tank Agora Industrie says that virtually all steel companies planning to build low-carbon steelmaking capacity at commercial scale are choosing hydrogen-based or hydrogen-enabled DRI plants rather than CCUS. is emphasized. His 2030 project pipeline of DRI plants has increased to 94 million tonnes per annum (Mtpa), while his commercial-scale CCUS pipeline with blast furnace-based operations will reach just 1 Mtpa.

In addition to unfortunately low recovery rates, CCUS for blast furnace-based integrated steel plants does nothing to address the methane emissions associated with metallurgical coal mining. According to the International Energy Agency, total methane emissions from coking coal mines worldwide reached 10.5 million tonnes (Mt) in 2023. This equates to up to 913.5 million tonnes of CO2 over a 20-year impact period. For comparison, his global CO2 emissions from steel production amount to about 2,800 tons per year.

Steelmakers around the world are already transitioning from coal-consuming blast furnaces to recycling steel in electric arc furnaces (EAFs) and DRI-based processes. Using green hydrogen in the DRI and renewable energy to power the EAF will enable the production of true low carbon steel. This is a feat that is unlikely to be repeatable with CCUS and has implications for long-term metallurgical coal demand.

Declining long-term outlook for metallurgical coal

The accelerating transition from blast furnaces to steel technology means the long-term outlook for metallurgical coal is changing.

The Australian Government's March 2024 Resources and Energy Quarterly Report (REQ) highlights that global trade in metallurgical coal is declining. According to forecasts, trade volume of 349 million tonnes in 2023 will decline to 333 million tonnes by 2029. Australia is currently the world's largest exporter of metallurgical coal, but Australian exports are projected to peak in two years and then decline until the end of the decade.

This doesn't seem like much of a product with a long and bright outlook, unaffected by changes in technology. Anglo American may be inclined to agree, but in contrast to BHP's belief that demand for metallurgical coal will continue for decades, Anglo said last year that the shift in steel technology from coal was only 10 to 15 years old. He said it was a yearly issue.

Scope 3 emissions impact

Anglo's long-term view on metallurgical coal is likely to have influenced its Scope 3 emissions approach. The company aims to reduce Scope 3 emissions by 50% by 2040.

In contrast, BHP has no measurable Scope 3 emissions targets. There is a 'target' to achieve net zero Scope 3 emissions by 2050, but as BHP explains, a target is not the same as a target.

One result of this potential acquisition could be the end of one of the more ambitious Scope 3 reduction targets among major mining companies.

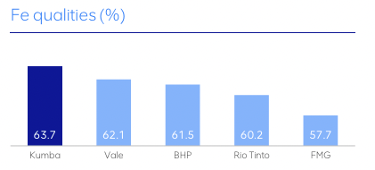

The high quality of Anglo iron ore further advances our Scope 3 objectives. The Minas Rio mine in Brazil produces low-carbon ore with high iron content suitable for DRI-based steelmaking (DR grade) and has significant expansion potential. Production from the Kumba iron ore operation has a higher iron content than most Pilbara production (Figure 1).

Figure 1: Comparison of Kumba iron ore quality and production of the four largest iron ore mining companies

Source: Anglo American Kumba Iron Ore

Kumba iron ore will be split up as part of the proposed takeover, likely because BHP wants to limit its exposure to South Africa and struggling rail logistics, while the Minas Rio mine will be split into BHP's blast-furnace-grade Pilbara operations. I'll probably add grade ores. .

BHP joins Rio Tinto and BlueScope Steel in exploring ways to make Pilbara ore suitable for DRI-based steelmaking, but so far, in contrast to other major iron ore mining companies Generally, there is no interest in developing DR grade mines with high iron content. .

In his recently released integrated report, Kumba points to “significant opportunities to reduce Scope 3 emissions” and emphasizes that “the demands on companies to manage their Scope 3 emissions are increasing…” Did.

The wholesale rejection of Woodside's climate plan by investors further emphasizes that point. Further expansion of the coal business and continued support for the sluggish and underperforming CCUS technology will put further pressure on BHP to take action on Scope 3 emissions.