KanawatTH/iStock via Getty Images

The following segment was excerpted from this fund letter.

Converge Technology Solutions (OTCQX:CTSDF, TSX:CTS:CA)

“If you’re going to invest in stocks for the longer term, there are going to be periods when there’s a lot of agony. I think you just have to learn to live through them.” -Warren Buffett

Converge Technology Solutions Corp. is a North American IT solution provider. They specialize in helping organizations modernize their IT infrastructure, leverage emerging technologies, and optimize their operations to drive business growth and innovation. Converge offers a wide range of IT services, including cloud solutions, cybersecurity, advanced analytics, digital infrastructure, and managed services.

In 2018, Converge went public with a strategy to consolidate small and medium-sized IT service providers (ITSPs). Initially successful, it attracted investors, including us, interested in both inorganic and organic business growth. However, in 2022, the M&A strategy faced challenges due to accumulated debt and a declining share price. Converge acquired well, but the problem was that it was not integrating these acquisitions and deriving revenue or cost synergies. Our initial mistake in this investment was believing that the management team was doing both things well.

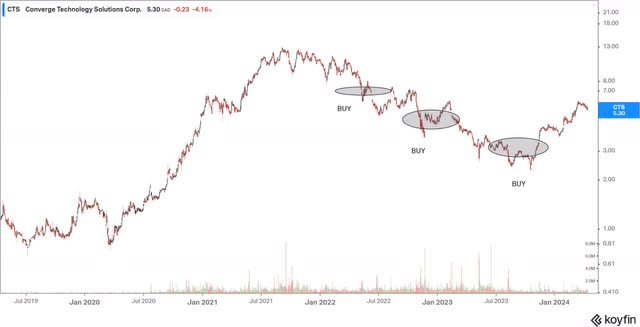

Value investors typically step in as a stock declines like this, however, Converge’s situation was complicated. The company had become a disparate collection of businesses through rapid M&A. In addition, Converge faced working capital problems. Capital tied up in working capital resulted in a lack of free cash flow, causing skepticism among value investors about reported earnings. There was also the issue of a reputed CFO departing just after a few months on the job! All this contributed to a decline in the stock price from C$12 per share in 2021 to a low of $2.3 per share in 2023 as there were no natural buyers of the stock.

At its bottom, it was trading for 3x EV/EBITDA. We held several meetings with management, including the new CFO, Avijit Kamboj, and determined that Converge is headed in the right direction. At that point, we significantly added to the position.

Since then, Converge has undergone significant changes, including putting the M&A strategy on hold. We anticipate improvements in free cash flow conversion in 2024, along with structural changes leading to margin expansion. The outlook for 2024 and 2025 includes modest revenue growth, margin expansion, and low double-digit earnings growth. Additionally, with better free cash flow conversion, Converge aims to deleverage its balance sheet and repurchase stock. We believe all this will lead to a re-rating and narrow the gap to intrinsic value.

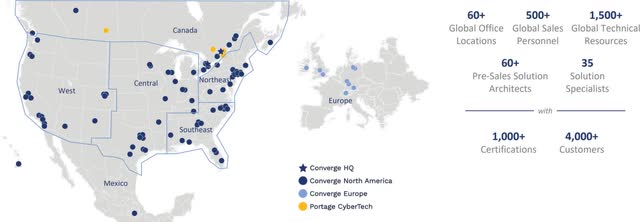

Business

In 2016, Shaun Maine incorporated Converge Partners to implement the roll-up strategy, targeting regional ITSPs in North America. In the beginning, the roll-up strategy at Converge, led by Shaun, generated significant shareholder value. Converge went public in 2018 and continued its M&A strategy. The idea was very simple: buy small ITSPs and derive synergies on cross-selling, costs, and managed services. Converge’s affiliated companies distribute a diverse array of products and solutions, encompassing standard hardware like laptops and mobile devices, business analytic software, AI solutions, blockchain solutions, cybersecurity software, public and private cloud solutions, data centers, networking, and storage products, among others.

Most of Converge’s existing customers are small-to-mid-sized enterprises or state/local governments.

Here is an overview of the business:

Source: Converge Presentation

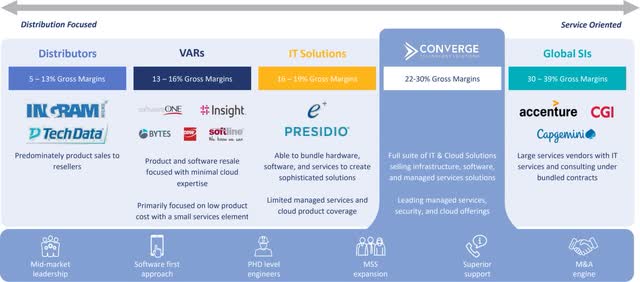

We have talked about IT services companies before with our report on EPAM. ITSPs bridge the gap between suppliers and customers in a highly fragmented environment. Customers struggle to select vendors and manage IT spending efficiently, while even large suppliers find it challenging to reach every customer effectively. The primary role of an ITSP is to provide outsourced distribution/sales for suppliers and outsourced procurement for consumers. For context, Converge, CGI, Accenture, and CDW boast extensive vendor relationships, along with a range of in-house solutions.

In addition to using ITSPs for procurement, many customers are increasingly turning to IT professional services for enhancing digital capabilities and implementing new IT products and services through project-based work. The growing complexity and diversity of IT solutions pose challenges for most non-experts.

Converge is a little different than full service IT services companies and contributes value to customers in three key ways:

- Offer software, hardware, and services either as resellers or directly.

- Provide project-based professional services encompassing design, configuration, integration, installation, and implementation.

- Offer ongoing managed services, essentially functioning as outsourced IT. This is the highest margin and most recurring revenue part of the business.

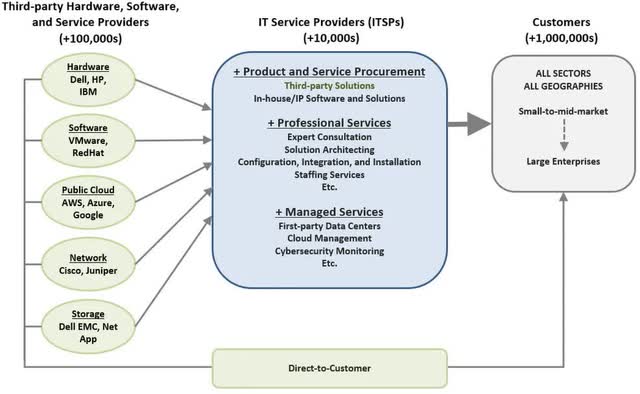

Managed IT services are gaining popularity as IT service providers take on ongoing responsibilities. Outsourcing IT functions to external experts proves cost-effective and reliable, especially for small-to-mid-market clients. For example, overseeing a customer’s cloud requirements, managing cybersecurity, managing networks etc. The key variables are uptime and how fast the IT services company responds to tickets or problems faced by the customer. Converge’s focus has now been on growing this part of the business. They have consolidated the operations in Mexico and standardizing processes so that they can increase the profitability of this division.

Source: 10th man deep dives

There is a really good report on Converge by ‘The 10th Man’. Anyone interested in reading in detail about the business, industry, M&A strategy should give that report a read.

The investment thesis is as follows:

Converge will increase margins by integrating the front and back end of all its acquisitions, thereby deriving synergies. In addition, free cash flow conversation will normalize that will then help Converge to pay down debt and buy-back stock. All these factors will force the market to re-rate the company closer to its peers.

“Our focus continues to be reinvesting back in our business, our innovations and on completing the integration of previous acquisitions, all in addition to paying down our debt and repurchasing our stock. We are capable of pulling several levers simultaneously with the cash we expect to generate from operations.”

-CFO (Q3 Earnings Call)

Margins

Converge was good at acquiring businesses, but was not very good at integrating them. A lot of its current problems stem from this fact!

The organizational landscape became increasingly complex as they focused on M&A. The acquisitions were made across verticals and across geographies. In fact, I would go as far as some acquisitions had no strategic rationale and were only made because they could be had for a decent multiple. Converge acknowledged challenges in encouraging Value-Added Reseller (VAR) salespeople to sell services. This issue is attributed to the relationship-oriented individual model, making it difficult to transition them into service-oriented sales roles.

Once M&A stopped and management understood that they had to execute for organic growth, they changed tack and started integrating the acquired companies.

“So our North America integration is the fastest integration continues to be on track. As I mentioned on last quarter’s call, our front office is primarily integrated with our back office as we’re working on this new ERP, which goes live mid next year, that’s where you’ll probably see the biggest synergies and operational efficiencies. We continue to look at how we’re going to integrate our European business, given that there are 2 separate restrictions. We are on a path to integrate the 2 businesses, distinct businesses that we bought in Germany into one Converge Germany.” -Greg Berard (Q3 Earnings Call)

Today, they are largely done integrating the front end. They significantly changed the sales organization and their incentive structure to align with the new priorities. The sales organization is now compensated on gross margins, cash conversation and sales of managed services. To provide some more detail, the current approach involves organizing regional structures led by VPs, with an emphasis on consolidating sales individuals within these structures. The transformation involves categorizing them into practice areas, enabling Converge to track the number of practice areas each sales representative is managing. Currently, 60% of sales reps are handling sales across four practice areas.

On the back end, Converge has decided to implement NetSuite as the new ERP solution. The primary objective is to unify all North American operations on a single, effective system. In addition, Converge will be able to seamlessly integrate and consolidate all relevant data for improved efficiency and accuracy in the operations.

The other factor that will help with margins is managed services. As we have mentioned before, the whole organization is now focused on growing the services, and specifically, managed services business.

“We want to get to $1 bn in managed services. We have 10K IBM reps selling our solutions. Most pure play do not have this channel. Mid-market companies cannot manage their network. Can we do it for you? Yes! Demand is very strong. We also do analytics on the cloud.” -Shain Maine (CEO)

In essence, the margin lift comes from,

- Front-end and back-end integration

- Higher proportion of professional and managed services

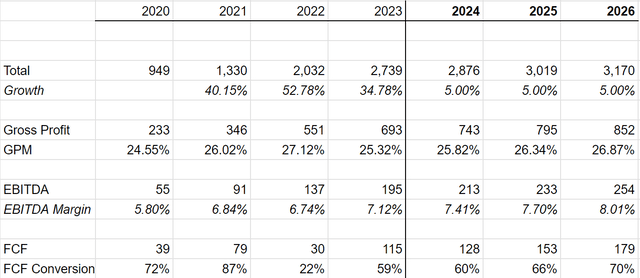

Converge has been making EBITDA margins of ~5-6% but has the potential to make margins of 7-8% over the longer term. We believe we will see snippets of this in 2024 with margins approaching 8% in 2025. Converge has made these margins in the past, and this will be in-line with its peer group.

Cash Conversion

Converge was a negative working capital company in 2020/21, but this flipped 180 degrees in 2022/23.

With so much M&A, there is always a risk that target companies inflated their revenues and that the actual cash from these revenues may not materialize. This remains a risk with Converge and some part of the revenue may never come back but, (A) Converge has not made a new acquisition recently and all past acquisitions have now been more or less integrated, and (B) Incentive structures have been changed and policies have been put in place to convert earnings into cash flow.

This cash conversion problem was made worse by the fact that Converge produced an ‘adj free cash flow’ metric. When a business has leverage on the balance sheet and needs to pay interest expense, then it can only be paid with real free cash flow and not ‘adj free cash flow’. I think the management understands this now.

Converge started compensating sales executives with payments tied to invoicing rather than cash receipts. However, there has been a recent shift in the commission structure. All incentives are now set to cash. To reinforce this, regional VPs regularly convene on calls, underscoring the importance of customer payments as a fundamental aspect of their operations. The message is clear: customers must fulfill their payment obligations. This is already bearing fruit, and Converge had a fantastic Q3 from a cash collection perspective.

“The snapback in cash generation this quarter was driven by moving swiftly to implement improved receivables and payables processes across the company with disciplined measures being put in place to better define terms and parameters for our contracts and operating hurdles for our operation. Implementation of these improvements is in progress and will continue.” -CFO (Q3 Earnings Call)

With maturation of acquisitions, new ERP, and change in incentives, we believe cash conversion will increasingly get better. The CFO has a target of 55-60% cash conversion between EBITDA and FCF, and we believe this number.

Financials

As we can see, FCF conversion suffered in 2022 and this was all due to the $77 mn in working capital. In addition, actual cash conversion also suffered from ‘one time items’ related to M&A and increasing interest expense as all of Converge’s debt is floating rate.

The net debt concluded the quarter at around $307.5 million, leading to a leverage ratio of 1.84x of TTM EBITDA. Converge has about $292 million in available capital encompassing cash reserves and the available capacity under the credit facility. It will likely use about 50% of its

FCF to pay down debt and the balance reserved for investments in the business and share buybacks.

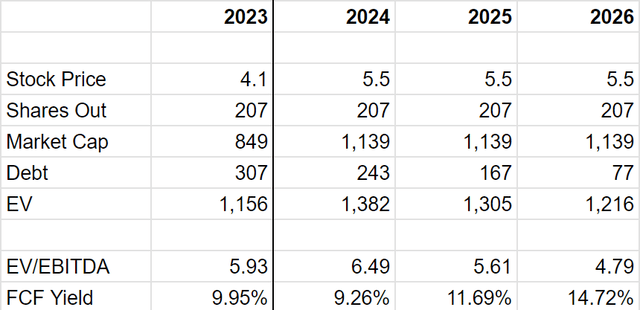

Converge is currently valued at 6.5x EV/EBITDA and we believe this is extremely cheap for the quality of the business. As investors realize that the cash conversion is real and as Converge pays down debt and buys back stock, we believe that the market will value Converge closer to 10x EV/EBITDA which means the stock can double in 3 years from these levels.

|

Disclosure: White Falcon has a long position in the shares of Converge. Disclaimer Past performance is not necessarily indicative of future results. All investments involve risk, including the loss of principal. It should not be assumed that any of the transactions or investments discussed herein were or will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the investments discussed herein. Specific companies or investments shown in this presentation are meant to demonstrate White Falcon’s active investment style White Falcon may change its views about or its investment positions in any of the securities mentioned at any time, for any reason or no reason. White Falcon disclaims any obligation to notify the market of any such changes. The information and opinions expressed in this presentation is based on publicly available information about the securities. The letter and thesis includes forward-looking statements, estimates, projections, and opinions, as well as more general conclusions. Such statements, estimates, projections, opinions, and conclusions may prove to be substantially inaccurate and are inherently subject to significant risks and uncertainties beyond White Falcon’s control. Although White Falcon believes the data and numbers are substantially accurate in all material respects, White Falcon makes no representation or warranty, express or implied, as to the accuracy or completeness of any written or oral communication. Readers and others should conduct their own independent investigation and analysis of the thesis of any and all companies mentioned in this document. The letter is not investment advice or a recommendation or solicitation to buy or sell any securities. White Falcon undertakes no obligation to correct, update, or revise the Presentation or to otherwise provide any additional materials. White Falcon also undertakes no commitment to take or refrain from taking any action with respect any of the companies mentioned in this letter. |

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.