Iron and Sea Technology Co., Ltd. (KOSDAQ:052860) had a very impressive month, with its stock up 26% after an earlier period of volatility. Looking back a little further, it's encouraging to see that the share price is up 28% in the last year.

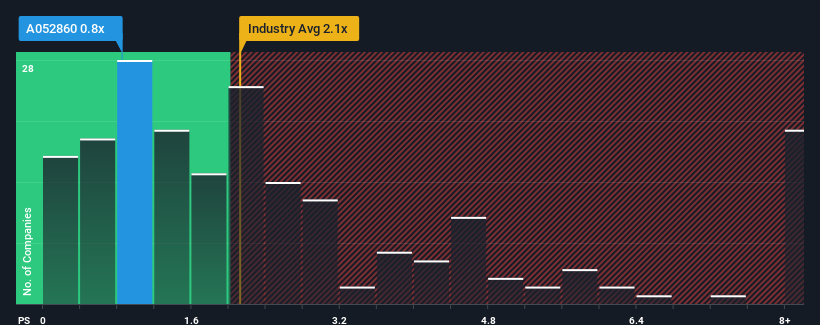

Even after such a large price increase, I&C Technology's price-to-sales (P/S) ratio is 0.8x, which makes us think it's a stock with a good investment outlook, considering the stock's price is almost 50%. If so, you can still understand it. The P/S ratio of companies in the Korean semiconductor industry is over 2.1 times. However, it is unwise to take P/S at face value as there may be an explanation as to why it is limited.

Check out our latest analysis on I&C Technology.

How has I&C Technology performed recently?

I&C Technology has certainly been doing a great job of growing its earnings at a very fast pace recently. Perhaps many are expecting the strong earnings performance to deteriorate significantly and the P/S ratio to be subdued. If you like the company, you'll hope it doesn't so you can potentially buy shares when the company is unpopular.

There are no analyst forecasts available for I&C Technology, but take a look at this. free Data-rich visualizations show how a company's revenue, revenue, and cash flow stack up.

Is revenue growth expected for I&C Technology?

The only time you can really feel comfortable seeing a P/S as low as I&C Technology's is if the company's growth is on a trajectory to lag its industry.

Looking back, the company achieved an unusual 63% increase in revenue last year. His most recent three-year period also saw an impressive 181% increase in overall revenue, helped by short-term performance. So it's safe to say that the company's recent revenue growth has been impressive.

Comparing recent medium-term earnings trends to the industry's one-year growth forecast of 95%, we find them to be significantly less attractive.

This information helps explain why I&C Technology is trading at a lower P/S than its industry. Apparently, many shareholders were reluctant to hang on to something they believed would continue to lag the rest of the industry.

Important points

Even though I&C Technology's stock price has increased recently, its profit and loss still lags behind most other companies. It has been argued that the price-to-sales ratio, while a poor measure of value in certain industries, can be a powerful indicator of business confidence.

Our research into I&C Technology shows that the company's revenue trends over the past three years have been below current industry expectations. This was confirmed to be the main factor. At this stage, investors feel that the potential for improved earnings is not large enough to justify a higher P/S ratio. Unless the recent medium-term situation improves, the stock price will continue to act as a barrier around this level.

Before you take the next step, you need to know the following: Two warning signs for I&C technology (1 is not very good to us!) We made it clear.

If you're interested in strong, profitable companies, you might want to check this out. free A list of interesting companies that trade at low P/E ratios (but have proven they can grow earnings).

Valuation is complex, but we help make it simple.

Please check it out I&C technology Could be overvalued or undervalued, check out our comprehensive analysis. Fair value estimates, risks and caveats, dividends, insider trading, and financial health.

See free analysis

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.