For the uninitiated, it may seem like a good idea (and an attractive prospect) to buy companies that tell investors a good story, even if they don't currently have a track record of revenue or profits. But in reality, if a company loses money every year over a long period of time, investors usually end up paying some of the losses. Investors should be careful not to put good money after bad money, as loss-making companies can act like sponges for capital.

So if this idea of high risk and high reward doesn't suit you, you might be more interested in profitable growth companies such as: Edarat Communication and Information Technology (Tadaul:9557). Profit is not the only metric to consider when investing, but it is worth evaluating companies that can consistently generate profits.

Check out Edarat's latest analysis on Communications and Information Technology.

How fast is Edarat Communication and Information Technology growing its earnings per share?

Even if growth rates are very low, a company is usually doing well if its earnings per share (EPS) are increasing year over year. So it's easy to see why many investors focus on his EPS growth. Edarat Communication and Information Technology's EPS jumped from €10.00 to €13.79 in just one year. This should be a result that will bring smiles to our shareholders' faces. That's a staggering 38% increase.

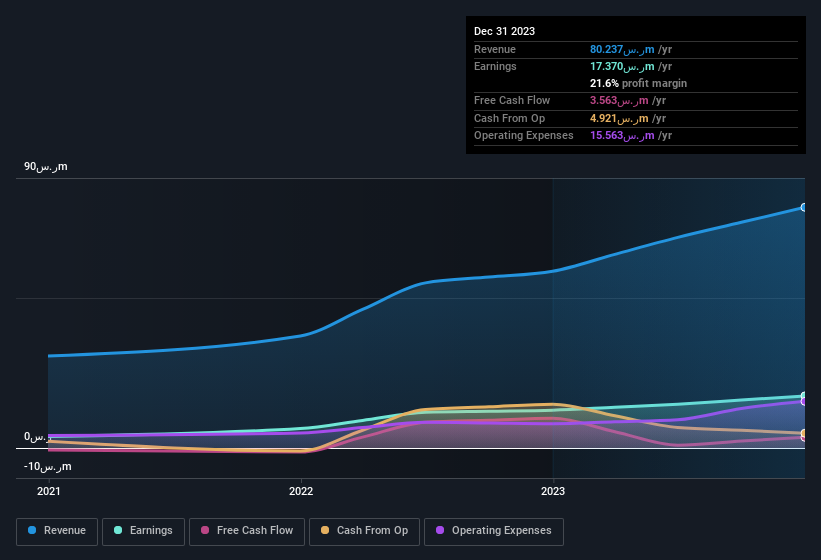

Revenue growth is a good indicator that growth is sustainable and, when combined with high earnings before interest and tax (EBIT) margins, can help a company maintain a competitive advantage in the market. This is an excellent method. Although Edarat Communication and Information Technology's EBIT margin remained almost unchanged from last year, the company is pleased to report that its revenue for this period increased by 36% to 60 million. That's a really positive thing.

You can see the company's revenue and profit growth trends in the graph below. Click on the image for more detailed information.

Edarat Communication and Information Technology isn't a very large company, considering its market capitalization of €668m. Therefore, it is very important to check the strength of the balance sheet.

Are Edarat Communication and Information Technology insiders aligned with all shareholders?

Insider investing is always reassuring to the market, as it requires company leaders to act in the best interests of shareholders. Followers of Edarat Communication and Information Technology will be relieved to know that insiders have significant capital that aligns the best interests of a broad group of shareholders. Specifically, they own 134 million worth of shares. That's a lot of money and no small incentive to work hard. As a percentage, this equates to his 20% of the shares outstanding for the business, which is a significant amount considering the market capitalization.

Should you add Edarat Communications and Information Technology to your watchlist?

There's no denying that Edarat Communication and Information Technology is growing its earnings per share at a very impressive rate. That's fascinating. This EPS growth is something the company can be proud of, so it's no surprise that insiders own a significant amount of shares. Rapid growth and confident insiders should be enough to warrant further investigation, making it seem like a good stock to follow. There is still a need to consider the ever-present concern of investment risk. We've identified 2 warning signs for you Understanding these should be part of your investment process.

Edarat Communications Information Technology certainly looks good, but if insiders have been buying up shares, it could become more attractive to more investors. If you want to see companies with insider buying, then check out this curated selection of Saudi companies that not only boast strong growth, but also have recent insider buying.

Please note that insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we help make it simple.

Please check it out Edarat Communication and Information Technology Could be overvalued or undervalued, check out our comprehensive analysis. Fair value estimates, risks and caveats, dividends, insider trading, and financial health.

See free analysis

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts using only unbiased methodologies, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.