morsa images

Investment overview

My Recommendations for Marvell Technology (NASDAQ:MRVL) is a buy rating. We believe the worst of the cycle is over for MRVL, and he should be able to enter an upward cycle and perform well as early as the second half of 2025. Growth accelerated in FY26. In the long term, MRVL's ability to continue to grow its data center business as MRVL occupies a leading position in 800g PAM4 optical solutions, which is a key driver for winning more AI deals. I think it's also bullish.

Business overview

MRVL is a supplier of a wide range of semiconductor technologies, including hard disk drive (HDD) and solid state drive (SSD) controllers, Ethernet switches, processors, and data center ASICs. A hardware platform and software that incorporates digital computing technology designed and configured to provide an optimized computing solution.like many companies The semiconductor industry's financial landscape is cyclical, having experienced three cycles in the past decade (the most recent downcycle began in FY2024). Each downturn resulted in significantly lower revenues and negative EBIT margins.inside latest quarter, MRVL reported 4Q24 revenue of $1.43 billion, with data center revenue of $765 million, carrier infrastructure revenue of $170 million, and enterprise networking revenue of $200 million. It reported $65 million in consumer revenue, $144 million in consumer revenue, and $82 million in automotive/industrial revenue. . Total revenue rose 1% last quarter and for the year, raising hopes for a turnaround in FY25. Adjusted gross margin also increased 330 bps sequentially to 63.9%, and EBIT margin improved from 33.1% to 33.8%.

Cloud infrastructure drives long-term growth.

I take sales and profit growth for the fourth quarter and full year of 2024 as a positive sign that the worst of this downcycle is over, and therefore look forward to the next upcycle and long term. We focus on the driving forces behind MRVL's growth. The main long-term tailwinds that I see right now are cloud infrastructure and AI, or MRVL's data center business. MRVL's data center business demonstrated incredible resilience and performance in Q4 2023, growing 38% sequentially and 54% annually to $765 million. AI was a key driver this quarter, driven by his MRVL's leadership position in 800G PAM4 solutions. This is expected to put MRVL in a good position to continue winning deals. There are several visible growth drivers supporting strong performance over the next 1-2 years (all of which will start contributing to earnings only at the end of FY25, providing a good foundation for FY26). is established).

- According to management, MRVL's next-generation 200G and 1.6T per lane PAM4 solution is beginning to be qualified by customers, with initial deployments expected to begin by the end of this year.

- In addition, management plans to increase implementation of PAM4 DSP for AEC and expects to ship products to many Tier 1 cloud customers this year.

- MRVL's next generation 51.2T switch is expected to ship later this year.

- Management also expects positive upside from increased investment in inference. In particular, MRVL has high demand for his next generation 800G DCI products and is currently shipping 400G DCI products in large quantities. Additionally, as his DCI customer base expands with successful designs at multiple data center customers, the revenue contribution from 800G DCI products is likely to increase further next year.

Another way to gauge MRVL's growth runway in the AI space is that AI is currently at the level of 'above 10%' of FY24 revenue, up from 3% in FY23. In just one year, the revenue mix has more than tripled, with run-rate revenue of $800 million ($200 million in Q4 2024). This is primarily due to MRVL's optical solution. In my view, the need for AI will not diminish in any way. In fact, I expect to see an acceleration in the future as companies around the world compete to acquire the best AI capabilities. To achieve this, the backbone (data storage and management) must be maintained at the same pace (or perhaps at a faster pace to allow for further development). Therefore, I expect continued long-term growth in his MRVL data center business.

Marvell Technology, Inc., a leader in data infrastructure semiconductor solutions, today announced Spica Gen2-T, the industry's first 5nm 800 Gbps transmit-only PAM4 optical DSP. Designed for transmit retiming optical modules (TRO modules), Spica Gen2-T reduces the power consumption of 800 Gbps optical modules by 40% while maintaining interoperability with traditional optical modules and IEEE 802.3-compliant host devices. You can save more than %1. MRVL

Apart from AI and data centers, I'm also optimistic about MRVL's cloud custom silicon business. MRVL is starting to grow towards his two customer acquisitions (first shipment he expects in Q1 2025) and will exceed his target run rate of $800 million by the end of 2024. Given that these designs are on track for significant increases in 2H 2025 and that management has a clear view of demand for both FY 2025 and his FY 2026, MRVL You should have no problem reaching it.

Other business outlook

As for the rest of the business, the Q1 2025 guidance suggests very poor performance, which I took very positively. Management is guiding for a 40% quarter-over-quarter decline in enterprise networking (up to 58% below peak in Q1 2025). Career consecutively he will decrease by 50% (Q1 2025 will be about 73% below the peak). and consumers are expected to decline by 70% sequentially (74% below peak in Q1 2025). For reference, these projected declines are the sequentially larger declines MRVL is expected to see over the past four years, indicating that negative demand/supply conditions are nearing an end. MRVL should soon show a strong recovery in demand. One positive data point for the turnaround is that storage is already starting to see a strong recovery.

We also benefited from incremental demand for our storage products as some of our data center end markets continue to recover. Revenue from Teralynx Ethernet switches also continued to increase during the quarter. Q4 2024

evaluation

Redfox Capital Ideas

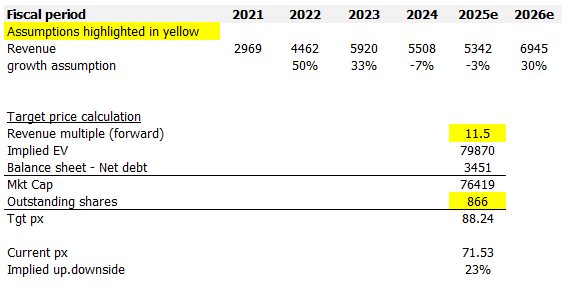

I model MRVL using a future earnings multiple approach, and based on my assumptions, I believe MRVL is worth $86.34. In my opinion, MRVL will see a significant growth acceleration for the next upcycle, which will likely be in FY26. This is because some business divisions will still be affected by the downcycle of the first quarter of 2025 (as mentioned above). ). It is difficult to pinpoint the exact recovery trajectory, but my assumption is that there will be a 3% decline in FY2025, and the extent of the decline will be small (some form of recovery will begin to be seen in the second half of 2025, but (offset by weaker performance in the first quarter). We should see significant acceleration in FY2026, which I estimate ~30% based on average performance over the past few cycles (28% growth in FY11, 19% growth in FY19, FY2022). is 50% growth). On an upcycle, MRVL should trade at a higher multiple given its stronger growth rate. The current forward earnings multiple is 11.5x, which is about 2.5x above the 2021 peak and about 3x above average. In my opinion, if MRVL shows stronger than expected growth, the multiple could surge to the previous peak, but the consensus is also for similar expectations (29.9% growth in FY25), so the current I think 11.5x better reflects my 30% growth forecast.

danger

I expect a short-term recovery, but it is difficult to pinpoint the exact timing of the tipping point and the pace of recovery. Historical data points can be helpful in making predictions, but there is no guarantee that they will be accurate. MRVL predicts several more quarters of economic slowdown, especially if the global macroeconomy is expected to be further strained by a prolonged period of high interest rates, raising the cost of capital for companies and thereby constraining investment budget space. is very likely to be expected.

conclusion

My opinion on MRVL is “buy”. MRVL appears to be nearing the end of its current downcycle, and I believe MRVL's leadership position remains well-positioned to take advantage of long-term growth in AI and cloud computing (data center business). I expect that. While the near-term outlook for some business segments remains weak, I expect a strong recovery in the second half of FY25. Risks lie in the precise timing and pace of the recovery, which may be influenced by macroeconomic factors.