iLeader Technology Co., Ltd. (SHSE:603533) has had a very successful month, rising 49% after a volatile period. Unfortunately, despite last month's strong performance, his 8.1% growth for the year isn't that attractive.

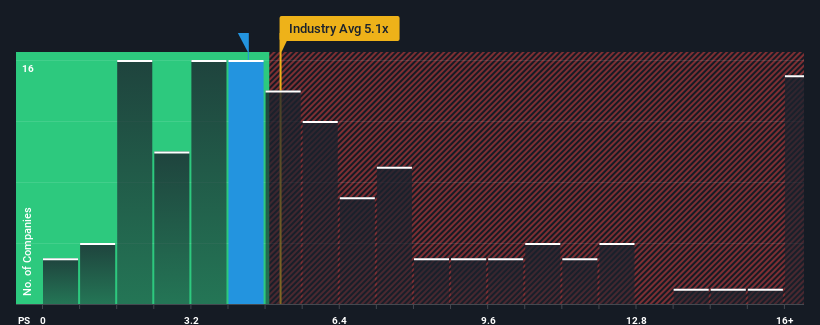

Even though prices are soaring, the median price-to-sales (or “P/S”) ratio in China's software industry is also close to 5.1x. But without a rational basis for the P/S, investors can miss clear opportunities and potential setbacks.

Check out our latest analysis on iReader technology.

How has IReader technology performed recently?

The revenue growth achieved by IReader Technology over the last year is probably more than most companies can tolerate. Perhaps many are expecting the respectable earnings track record to wane, and that may be holding back the P&L from rising. Those who are bullish on IReader Technology hope otherwise and can pick up the stock at a lower valuation.

There are no analyst forecasts available for IReader technology, but take a look at this. free Data-rich visualizations show how a company's revenue, revenue, and cash flow stack up.

Is revenue growth expected for IReader technology?

To justify its P/S ratio, IReader Technology will need to grow in line with the industry.

Looking back, the company's revenue grew by 15% last year. Pleasingly, thanks in part to growth over the past 12 months, revenues have also increased by a total of 35% compared to his three years ago. So we can start by seeing that the company has done a great job of growing its earnings over that period.

Comparing recent medium-term earnings trends to the industry's one-year growth forecast of 30%, we find them to be significantly less attractive.

With this in mind, it's interesting to see IReader Technology's P/S is in line with the majority of other companies. Apparently, many investors in the company aren't as bearish as they've been made out to be lately, and aren't looking to exit the stock anytime soon. They may be setting themselves up for future disappointment if P/S falls to a level commensurate with recent growth rates.

What can we learn from IReader Technology's P/S?

IReader Technology's stock has had a lot of momentum lately, with its P/S level being on par with other companies in the industry. Generally, we prefer to limit the use of price-to-sales ratios to establish what the market thinks about a company's overall health.

We find that IReader Technology's average P&L is a bit surprising, as its growth rate over the last three years has been lower than the overall industry forecast. When we see slower growth and weaker earnings than the industry, we think the stock is at risk of falling and the P/S is in line with expectations. Unless recent medium-term conditions improve, it is difficult to accept the current share price as fair value.

It is also noteworthy that we discovered 2 warning signs for iReader technology (1 is important!) Must be considered.

If you're interested in strong companies that are profitable, then you might want to check this out. free A list of interesting companies that trade at low P/E ratios (but have proven they can grow earnings).

Valuation is complex, but we help make it simple.

Please check it out iReader technology Could be overvalued or undervalued, check out our comprehensive analysis. Fair value estimates, risks and caveats, dividends, insider trading, and financial health.

See free analysis

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts using only unbiased methodologies, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.